Omise AI

AI-powered efficiency

“How money moves is becoming as critical as how much.”[1] This perfectly captures the payments industry in the several years to come. With the rise of AI-driven technology that adds new levels of intelligence and autonomy, the way money moves won’t be the same. As a result, 2026 is set to be a year of transformational change across the payments and fintech landscape, changes that will influence how businesses operate and how customers pay.

So, what do you need to know to stay ahead? Here’s what’s shifting for the people who use, build, and lead payments.

AI is making payments smarter and faster, and every provider is raising the bar for convenience and seamless experiences. What customers once considered ‘great’ is now the bare minimum. For businesses, this isn’t just a challenge; it’s an opportunity to stand out, win loyalty, and turn every transaction into a competitive advantage.

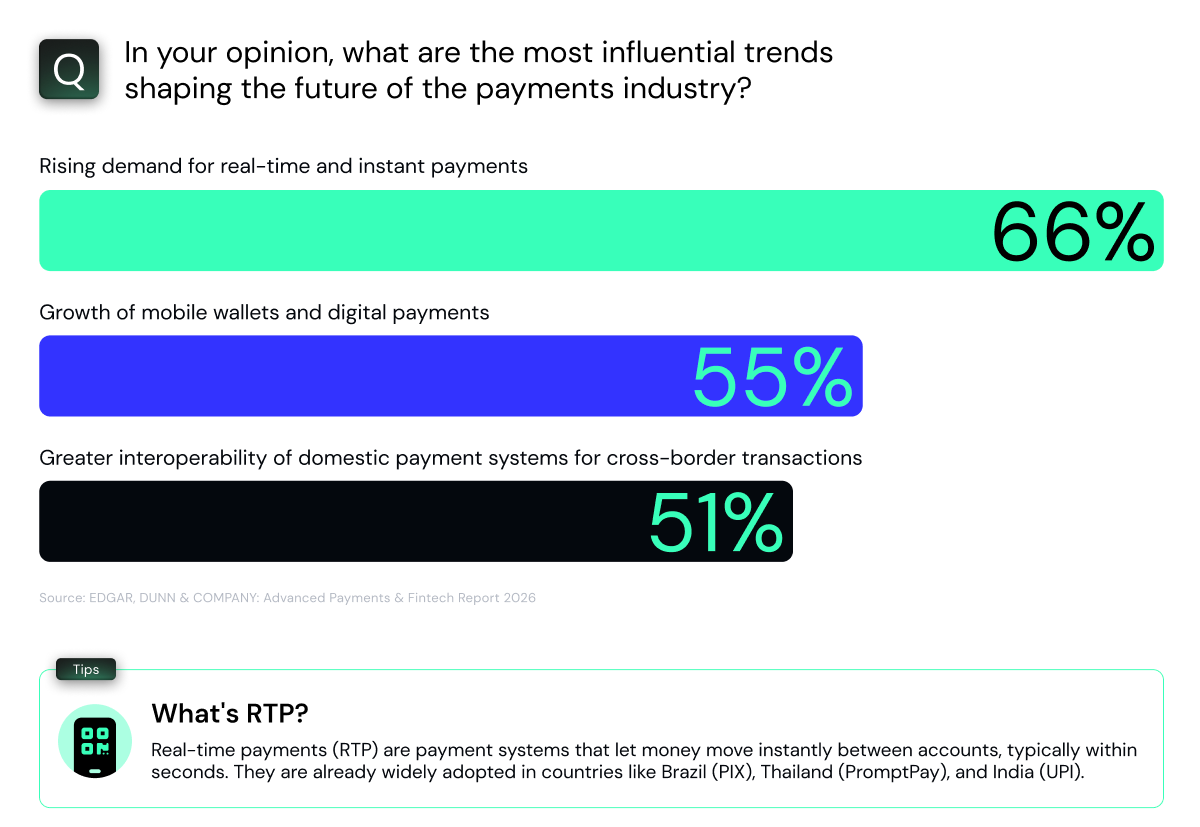

Alternative Payments Are a Must-Have

Digital wallets, BNPL, and real-time payments (RTP) are no longer optional, they are essential for businesses to stay competitive. A Fintech report from Edgar, Dunn & Company interviewing over 50 senior payments professionals across the globe have found that the rising demand for real-time payments will be the most influential trend shaping the payments industry (66%), followed by mobile wallets (55%) and cross-border interoperability (51%)

Checkout Moves Upstream

Social media was once mainly for connecting and discovery. Now it’s evolving into a commerce platform itself (TikTok Shop, for example). Checkouts are embedded directly into content, letting users buy mid-scroll without leaving the platform, and creating a seamless journey from engagement to purchase.

Agentic Commerce: AI Now Shops for Your Customers

AI agents can now autonomously shop for users, handling everything from browsing and comparing products to checking stock and making payments, all within a single conversation, without the customer leaving the chat.

In fact, 81% of consumers expect to shop using agentic AI, and several big players, like Amazon (‘Buy For Me’) and Google (‘Shop with AI’), are already starting to implement this. It is no longer theoretical or experimental, but is becoming increasingly practical.

For merchants, this means stores must be “agent-friendly” as well as customer-friendly, optimizing for both human and AI shoppers. For instance, this could involve making your data agent-readable, enabling API-first checkout solutions, minimizing steps that require human input, or even deploying your own branded agents so they can interact agent-to-agent (A2A).

(Read more on Agentic Commerce here.)

Creating a Frictionless Experience

Frictionless and seamless have been repeated across the payments industry for years, and for good reason. A checkout journey without hurdles still drives customers to complete their purchase and return again. In fact, 91 percent of U.S. consumers say a smooth checkout influences repeat business[2]. Industry experts also believe frictionless checkout will continue to fuel e-commerce growth in the next three to five years, with 76 percent viewing it as a top driver. Retailers that prioritize it will gain a clear competitive advantage.

With AI, payments can become even smoother at every touchpoint. For example, authentication can be enhanced by allowing trusted shoppers, identified through historical behavior, to skip unnecessary verification steps. Dynamic payment method selection can also tailor the checkout experience by showing each customer the options they are most likely to use. These small, intelligent adjustments work together to create a more frictionless experience for every shopper.

Payments in 2026 aren’t just a cost of doing business, they’re becoming a strategic advantage. The right payment strategy can drive revenue, reduce risk, and make operations more efficient.

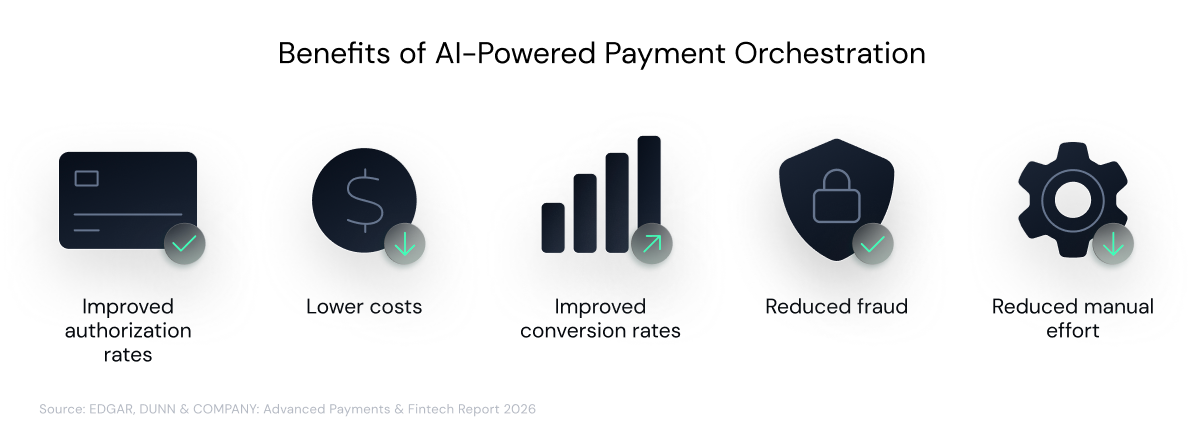

Payment Orchestration, Powered by AI

In the past, transactions were processed in a one-size-fits-all way. This meant businesses had no way to optimize their routes or reduce costs, leading to high processing fees (averaging 2.4% for credit cards) and poor acceptance rates. But as AI increasingly becomes a core engine in payment orchestration, especially in intelligent payment routing, AI agents are adaptive and efficient in decision-making; they can learn and act autonomously in real time. For example, AI can select the optimal route for each transaction based on real-time data, increasing approval rates while keeping costs low.

Beyond efficiency, AI-powered payment orchestration can also strengthen risk management. It can detect emerging fraud patterns and reroute transactions to safer, better-performing gateways.

Payments as Revenue Engines

We’ve been talking about how payments can create revenue for many years now. If you’re new, well, basically, platforms that own their checkout, embedded payments, and value-added services can earn extra income from each transaction.

But in 2026, as technology and AI become more mature, AI is now helping reduce operational costs by enabling things like dynamic fee optimization, risk-adjusted routing, and hyper-personalized payment methods. Businesses can unlock new streams of income while improving the customer experience at the same time.

(Read how Omise can level up your business with embedded payment here.)

Since AI drastically lowers the complexity of being a PayFac, it is a good time for SaaS platforms to have embedded payments and offer value-added services. This way, they can earn more profit. A BCG survey across five European markets and 4,500 US SMBs found that roughly half of the merchants who switched payment service providers in the past two years adopted embedded payments through their software platform because of ease of use and better support.

Thus, scaling is still important for businesses like SaaS platforms, marketplaces, and e-commerce platforms, but gaining extra while doing so will help them go further.

Autonomous Onboarding and Compliance

In the past, ensuring safety and completeness meant processes naturally moved slowly—so merchant onboarding often took weeks or even months. Now, with AI, speed and security can go hand in hand.

With the arrival of standard protocols like MCP (Model Context Protocol), multiple AI agents can work together seamlessly to streamline onboarding. For example:

These AI agents can communicate and collaborate automatically, sharing relevant data and decisions. For instance, once an identity agent verifies a merchant, the compliance agent can immediately proceed with regulatory checks, while the risk agent evaluates operational risk, all without manual intervention. The result is a faster, more accurate onboarding process that reduces friction for new customers while keeping the business fully compliant.

Payment providers are racing to develop the most advanced, AI-driven systems in the industry. What will set the winners apart is not just the intelligence of their technology, but their ability to earn trust while keeping experiences simple, seamless, and borderless. The leaders are those who create infrastructure that is adaptive, transparent, and intelligent by design.

Autonomous but Accountable

According to a KPMG study on attitudes toward AI in 2025, more than half of people globally are still unwilling to trust AI. This hesitation could be even higher when it comes to letting AI handle payments.

For payments, transparency and explainability are critical to ensuring that both users and regulators can trust the system, especially as AI increasingly acts autonomously on behalf of users, making decisions, handling sensitive data, and completing transactions. Builders, therefore, need to design platforms that are not only intelligent, but also transparent, reliable, and easy to understand.

Simplicity is Key

Each provider is racing to embed more intelligence into their platforms. But as capabilities grow, complexity often grows with it. Whether it’s banking apps, payment dashboards, or enterprise financial systems, the real challenge for builders is delivering smarter systems that still feel simple.

This goes beyond interface design. It’s about structuring workflows, automation, and decision-making logic so that users experience clarity, not confusion. When systems are intuitive at every layer, customers feel more in control.

Interoperability and Programmable Compliance from Day One

The future of payments won’t be built on isolated systems. It will rely on infrastructure that can adapt, connect, and operate across regions, currencies, and rails. Builders need to design platforms that support true interoperability so cross-border, multi-rail transactions feel as natural as any local payment.

The same applies to compliance. Every country has its own rules, and those rules evolve. Instead of relying on manual checks or rigid rule books, next-generation platforms must embed compliance directly into their architecture. Policy engines should be modular, switchable, and configurable to each region, with updates applied automatically rather than requiring a full system rebuild.

Emerging technologies are shifting the payment landscape like a row of dominoes, transforming how people pay, how businesses accept money, and how providers build solutions. Although these trends offer a glimpse of what’s ahead, the unexpected is always around the corner. (And sometimes, it jumps at you without warning.)

The best way to stay ahead? Stay flexible and ready to embrace change.

Sources

McKinsey & Company. (2025). The 2025 McKinsey Global Payments Report: Competing systems, Contested Outcomes. https://www.mckinsey.com/industries/financial-services/our-insights/global-payments-report#/

Pymnts. (2023, May 16). Merchants offer dozens of features to get shoppers to buy, here are the 10 that matter. PYMNTS.com. https://www.pymnts.com/news/ecommerce/2023/91-percent-ecommerce-shoppers-say-smooth-checkout-inspires-repeat-business/

Edgar, Dunn, & Company. (2025). Advanced Payments & Fintech Report 2026. https://www.edgardunn.com/reports/advanced-payments-and-fintech-report

Boston Consulting Group. (2025). FINANCIAL INSTITUTIONS GLOBAL PAYMENTS REPORT 2025: The future is (Anything but) stable. https://web-assets.bcg.com/25/91/2269153c468ca43684442f055cb0/2025-global-payments-report-sep-2025.pdf